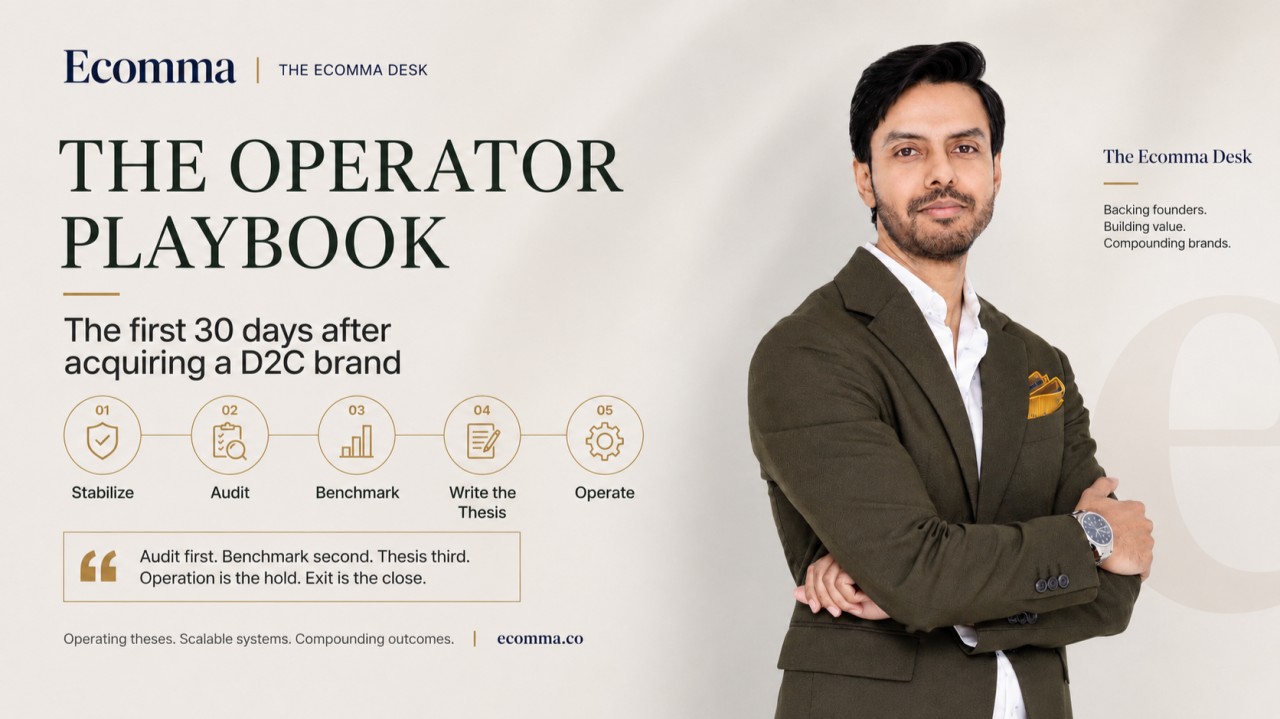

The operator playbook for the first 30 days after acquiring a D2C brand

The operating sequence we run in the first 30 days of a hold.

The first 30 days after close reveal whether the acquisition thesis can survive daily operations. Pre-close work is pricing. Post-close work is operating. The gap between a good price and a good deal gets filled by the sequence of decisions made after handoff.

A Bain & Company study of process and systems integration reports that 70 percent of process and systems integrations fail at the beginning, not at the end. That is an integration finding, not a claim that 70 percent of acquisitions fail or that they fail within 30 days. The relevant lesson is to define the integration thesis early and sequence the work deliberately.

We operate every brand we acquire. That is the model. A broker lists and walks. A fund of funds allocates and monitors. We hold the asset through its full lifecycle. Acquisition is the entry. Operation is the hold. Exit is the close. The operate phase begins the morning after close.

The operator playbook we run is a sequence. Stabilize the base business first. Audit the base business: start with unit economics, then widen to customer data and supply chain exposure. Then benchmark the paid engine against its replacement cost. Then write the integration thesis that the rest of the hold pays off. Skip the sequence and the hold bleeds value before the first board update.

Why the integration thesis starts in the first 30 days

Bain's research links repeatable M&A capability with stronger long-term returns and identifies an explicit process-and-systems integration thesis as the first of six practices used by high-performing acquirers. The practical implication for a smaller ecommerce acquisition is the same: establish the fact base, choose what will be integrated, and decide what can continue independently before transformation work begins.

A new owner can instead launch new channels, renegotiate suppliers, restructure the team, and rebrand the store in the first month. Each idea may be defensible in isolation. Attempting them simultaneously creates organizational chaos inside a business that was profitable enough to buy.

FE International's 2026 ecommerce M&A overview describes buyers stress-testing unit economics, supply-chain exposure, and customer data quality during diligence. The same areas deserve attention in the post-close audit. Diligence surfaces the headline risk. The first 30 days of operating surface the operational reality underneath it.

In a DTC supplements brand we acquired, diligence flagged channel concentration heavily weighted toward Meta paid. The flag was accurate. What diligence did not surface was that the founder had verbal supplier agreements with a factory that could shift production terms on short notice. The operational risk under the financial risk was the actual exposure. We found it in the first week of the audit. That is what the first 30 days are for.

The first 10 days are an audit, not a transformation

We do not touch the revenue engine in the first 10 days. We audit it. The temptation to optimize immediately is the most common operator mistake, and it is expensive. A paid-media manager who inherits a sizeable monthly Meta budget on day one wants to restructure campaigns by day two. A new GM wants to renegotiate the 3PL contract by day three. Both impulses are correct about the problem and wrong about the timing.

The first 10 days surface three realities. Unit economics of each SKU comes first. Revenue mix by channel comes second, including how much of it is founder-dependent. Supply chain exposure comes third, meaning which supplier relationships are documented and which remain verbal.

Our Operate-Lift Map framework sequences this work deliberately. Quick wins in the opening weeks include channel optimization and supplier renegotiation. Expense rationalization follows. The quick wins come after the audit, never in place of it. You cannot optimize a channel you have not benchmarked. You cannot renegotiate a contract you have not read.

The FE International overview reports a 24.7 percent year-over-year rise in DTC customer acquisition costs in 2025. That makes paid-media efficiency an important lever in the post-close window. But the benchmark that matters is replacement cost from a cold start, not historical spend. If a brand is running at a blended CAC that a new entrant could not match, the paid engine has real value. If the blended CAC is only achievable because of accumulated creative assets and audience data that the prior operator built over years, the engine is more fragile than the P&L suggests.

We benchmark CAC-to-LTV in the first 10 days using the brand's own cohort data. When cohort data does not exist, the first 10 days include building it. That is slower than restructuring campaigns. It is also the difference between operating on evidence and operating on assumption.

Days 11-20: Benchmark the paid engine to its replacement cost

By day 10, the audit has surfaced the actual unit economics, the actual channel mix, and the actual supply chain exposure. Days 11 through 20 are when we benchmark the paid engine against its replacement cost and decide what to keep, what to restructure, and what to shut down.

The replacement-cost question is the one most operators skip. A brand spending heavily on Meta paid with a strong blended ROAS looks healthy. The same brand, benchmarked against what it would cost to rebuild that ROAS from a cold creative library and a cold pixel, tells a different story. Accumulated creative assets, years of pixel data, and lookalike audience depth are invisible balance-sheet assets. They are also the assets that depreciate fastest if the operator stops feeding them.

In an Amazon-FBA outdoor gear brand we acquired, the paid engine was Amazon itself. Revenue ran almost entirely through a single marketplace. The temptation was to build a DTC store immediately. We did not. The deal thesis was that Amazon was the primary engine and the operate work was building optionality around it, not replacing it. We benchmarked the Amazon engine to its replacement cost and found it was more efficient than any DTC build we could stand up in the hold period. The operate work went into email list building and product diversification instead.

Typical industry guidance suggests benchmarking CAC-to-LTV ratios in the range of 1:3 to 1:5 within the first 20 days. That range is a starting point, not a verdict. Subscription businesses with high repeat-purchase rates operate at different ratios than single-purchase DTC brands. The benchmark matters less than the discipline of computing it from actual cohort data rather than from blended platform reports.

The output of days 11 through 20 is a paid-engine memo. It states what the engine is doing today, what it would cost to replace, what is driving the efficiency, and what the operator should do about each of those three findings. That memo becomes an input to the integration thesis in the next phase.

Days 21-30: Write the integration thesis, not the to-do list

Bain's research found that winning acquirers focus the integration on a short list of key value drivers. They do not resolve every internal complexity. They pick the three or four levers that will move enterprise value most and sequence the rest behind them.

Days 21 through 30 are when we write that list. The integration thesis is a document, not a feeling. It names the specific value drivers the hold will pursue, the evidence behind each one, and the sequence in which the operate team will execute. Items that do not make the list get deferred to quarter two or later.

The thesis draws directly from the audit and the paid-engine memo. If the audit surfaced that founder-dependent supplier relationships are the primary risk, the thesis leads with supplier formalization. If the paid-engine memo showed that creative asset depreciation is the hidden exposure, the thesis leads with creative production pipeline buildout. If the audit showed that the brand has no cohort LTV data segmented by acquisition channel, the thesis leads with data infrastructure.

Our thesis on owned-audience density is relevant here. Consensus says diversify channels so no single source exceeds 60 percent. Our view is that 60/30/10 is the floor and the actual edge is owned-audience revenue density: 25 percent or more from email, SMS, and organic, backed by named cohort LTV. Two brands with identical channel splits price differently when one has named LTV cohorts and the other has only blended numbers. The integration thesis should name the owned-audience target and the data infrastructure required to prove it.

In a subscription beauty box brand we acquired, the integration thesis led with founder replaceability. Repeat-purchase revenue was the premium driver behind the acquisition multiple. The risk was that creative direction and brand identity lived in the founder's head. The thesis named creative-director hire, supplier exclusivity formalization, and social-channel migration as the three value drivers. The rest deferred. That discipline is what kept the hold focused.

Channel diversification inside 30 days is a category mistake

The most expensive mistake we see in post-close operating is attempting channel diversification in the first 30 days. Channel diversification is a later-phase initiative. It requires the audit complete, the paid engine benchmarked, and the integration thesis written. Starting it in week one produces a half-built second channel, a neglected primary channel, and a P&L that degrades on both ends.

The category mistake is treating diversification as a risk-reduction move. Diversification is a value-creation move. It adds to the multiple at exit because it demonstrates owned-audience density and reduces buyer concentration risk. But it adds to the multiple only when the second channel is proven, meaning it has revenue, not signups. A large email list with no attributed revenue is a marketing asset. A large email list with tracked cohort revenue is a multiple driver.

In the DTC supplements brand we acquired, channel diversification was the core operate thesis. We built email and SMS to a point where they contributed a meaningful share of new-customer revenue. That work took months. It did not start in the first 30 days. It started after the audit confirmed that Meta paid was the concentration risk, after the paid-engine memo confirmed that the Meta engine had replacement value worth preserving, and after the integration thesis named owned-audience buildout as the primary value driver.

In the Amazon-FBA outdoor gear brand, we did not diversify the channel mix. We built optionality. A substantial email list of active subscribers added measurable value at exit even though the channel itself contributed a small share of revenue. The buyer saw proven optionality outside Amazon, not aspirational signups. That distinction is what the 30-day audit and thesis phase is designed to surface.

The sequence matters. Audit first. Benchmark second. Thesis third. Diversification fourth. Reorder the sequence and the hold pays for it.

A 30-day operator is the counterparty a buyer finances

The brands that clear upper-band multiples have an operator who has run the business independently for 30-plus days before going to market. Buyer IC memos cite this as the most common confidence factor. Evidence that the founder has been removed from daily decisions and the business continued to perform is what separates a clean close from a drawn-out diligence cycle.

The 30-day operator playbook we run in the hold phase is the same discipline a seller should run before listing. Stabilize. Audit. Benchmark. Write the thesis. Execute the short list. Defer the rest. A seller who does this before going to market arrives with the evidence buyers price into the multiple: documented unit economics, benchmarked channel efficiency, a written integration thesis, and a track record of operator-run performance.

We acquire on cash-on-cash payback. We operate through Product and Marketing. We exit when the multiple is set. The operate phase is where the multiple gets set, and the first 30 days of operate are where the trajectory locks in. A brand that enters the hold with a clean audit, a benchmarked paid engine, and a written thesis compounds value from day 31 forward. A brand that enters the hold with a restructured campaign manager and a half-built email list spends quarter two recovering from quarter one.